Diving into the racial wealth gap — understanding our nation’s deep history.

The rising inequality that exists within America started with the policies implemented by our very own government.

By definition, the term wealth gap, is the “the widening gap between America’s wealthiest and its middle and lower classes.” But when we speak about the wealth gap, it would be unfathomable to ignore any mention of race. This “widening gap” exists because of systemic racism, and the ramifications of these discriminatory policies that have pervaded our nation’s deep history are still alive and thriving today — the median wealth of a white family is ~$171,000, while for African-Americans it’s only ~$17,000.

So how did we get to where we are today?

Less than 200 years ago in America, slaves used to be printed on money — the same areas today where we hold the faces of U.S. Presidents. Unlike our presidents, the slaves weren’t being glorified.

This was a perpetuating reminder that the only purpose that black people served in America was to perform slave labor. Not only were they a physical representation of wealth, but they actually were the backbone of the economic system. By the time slaves were freed in the 1860s, they were generating over $3.5 billion of economic value, thus making them the “largest single financial asset in the entire U.S. economy, worth more than all manufacturing and railroads combined.” When the freedom bells finally rang, President Lincoln approved a bill that promised 40 acres of land to each family of freed slaves. This was estimated to set aside 400,000 acres of land for over 4 million families, an estimated economic value of over $6.4 trillion dollars in today’s worth. However, after he was assassinated, the bill was quickly revoked and thousands of slaves were evicted from their land. This was a major turning point that normalized the idea that black people don’t deserve to own property.

African-Americans have been barred from owning property for generations.

Owning property in America is the most influential factor in building generational wealth. Approximately two-thirds of all of the wealth of America’s middle class families comes from home ownership. This is because the wealth that properties generate for families grows over time with compounding interest. This is the idea that if I invest $100 today, then in 10 years, not only will my principal investment gain interest, but the interest that I gained on the principal will gain interest. To put this into perspective, you should realize that a $100 bill in 1863, is worth about ~$2,000 today. However, if you were to have invested that same $100, taking advantage of compounding interest, it would be worth over $3.5 million today.

The status quo of black people not having the right to property has induced some of the greatest tragedies that have affected our communities. These are the underlying motivations behind the massacre of Black Wall Street and federal processes such as redlining.

“This ‘widening gap’ exists because of systemic racism, and the ramifications of these discriminatory policies that have pervaded our nation’s deep history are still alive and thriving today.”

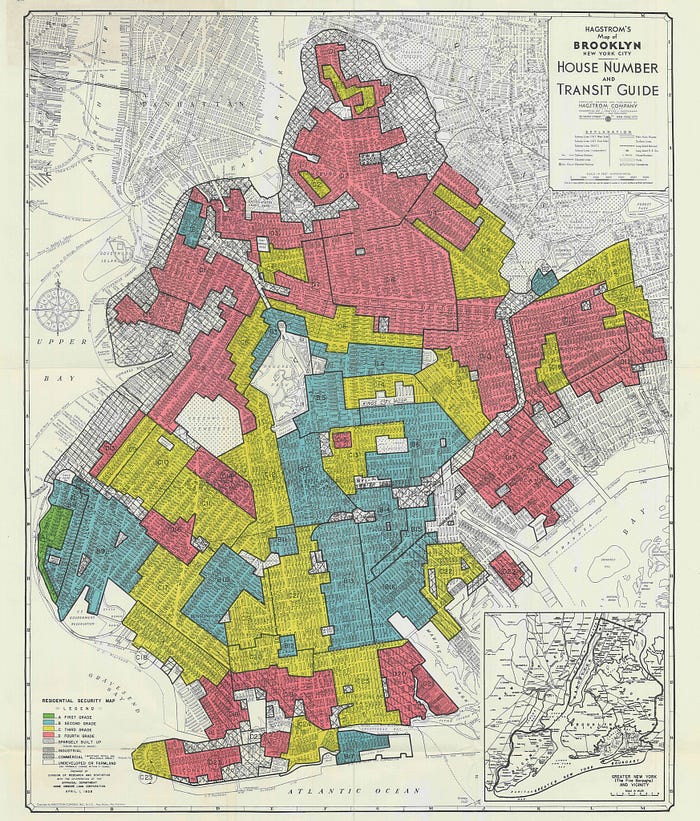

After the great depression, President FDR released over $100 billion dollars of funding in the form of mortgage credit to give Americans the opportunity to own their homes. This brought to life the idea of the “American Dream.” After one of the worst economic periods our country has ever faced, the opportunity to own a home was invaluable. But there was one small caveat. During the implementation of these policies, the Federal Housing Administration (FHA) decided that they wouldn’t give credit to any homes located in areas deemed to be “risky.” So how did they calculate which areas were risky? African-American neighborhoods. The result? 98% of the loans that were issued during this period were given to white families.

When we speak about the term “redlining,” it’s not just a mere figure of speech. The FHA would actually draw maps with entire neighborhoods marked in red where African-Americans lived. They then agreed to not ensure any of those homes. Thus, not only could African-Americans not afford to own the homes in their own neighborhoods, but they couldn’t move into white neighborhoods because that would bring the property values down. These policies were so entrenched in the system that even real estate agents could get their licenses revoked if they were found to be integrating neighborhoods.

The negative feedback loop of racist policy

“Racism begets more racism.” All of this began with policy that governed who can participate in home ownership — discriminatory practices against African-Americans. Essentially, federally enforced segregation. This gave birth to the pernicious effects of racism: low property values in African-American neighborhoods; businesses not willing to operate in those areas; low funding for public schools and programs; higher rates of crime and incarceration. I could break off the multitude of byproducts into an entire essay. All of these outcomes of racism then stack on top of each other and give rise to more racism. People see the current affairs of African-American life in a vacuum and give damaging comments: “African-Americans are just low achievers”; “most of them don’t even graduate from high school. They’re lazy”; “Look at their incarceration rates. They’re criminals.”

As a whole, African-Americans weren’t given access to mortgage credit up until the 1990s. However, because they weren’t financially literate, they had no idea that banks were engaging in predatory lending techniques with them at much higher rates than any other race. Instead of getting the same types of federally subsidized loans that FDR issued during the New Deal, they were getting subprime loans. It didn’t matter if you had a perfect credit score. Put simply, subprime loans are made to seem attractive because they start out either extremely cheap or free. However, the interest payments eventually compound at vicious rates — ones that African-Americans couldn’t possibly afford to pay back. As a result, when the housing market crashed in 2008, black communities lost over 53% of their wealth.

“When we speak about the term “redlining,” it’s not just a mere figure of speech.”

Why the wealth gap is systemic.

The reason that we use the word “systemic” when we talk about racism and the wealth gap is because the policies that discriminate against African-Americans were inscribed by the very same government that we have today. As a country, if we can ever dream about closing the wealth gap, we first have to truly understand and admit to the historical context behind it.